Dentistry UK Market Report 6ed

Who the report is for

- Dental practices and dental groups

- NHS Commissioners

- Banks

- Private equity investors

- Management consultants

- Business advisors

- Insurers and insurance brokers

- Central Government

- Think Tanks

- Policy Writers

What the report includes

- Market Overview

- ‘High street’

- NHS

- Corporate

- Dental plans

- Politics and Policy

- Regulation and Representation

- NHS Funding

- Dental Provision

- Staff Recruitment, Training and Retention

- Private Dentistry

- Corporate Dentistry

- Investment in UK Dentistry

- Appendices

- Glossary

- Regulators

- Trade Bodies

- Major Provider Profiles

- Financial appendix

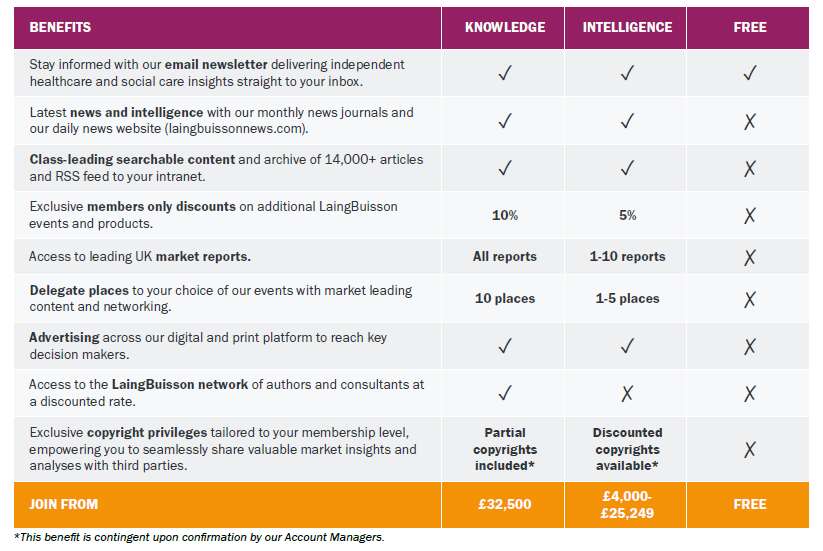

What You Get

- Print package – Single-user Printed Hard Copy

- Digital package – Multi-user Digital PDF and Microsoft Excel files + Printed Hard Copy

Want to know more? Our sales team can help.

Call: 020 7841 0045

Email: [email protected]

Will dentistry demand return to pre-pandemic levels?

The report shows a ‘High Street’ dentistry market, valued by LaingBuisson at £8.3 billion in 2020/21, which shrunk nearly 10% in real terms (after taking account of CPI) since the previous year. Of this, private sector dentistry accounted for £4.6 billion, while NHS spend amounted to £3.7 billion.

This new edition of the Dentistry UK Market Report evaluates the significant impact of the Covid-19 pandemic on the fragmented market. During 2020, much routine treatment ground to a halt, and when combined with the restrictions on aerosol generating procedures, only very urgent and emergency treatments could take place.

Updated figures show that demand decreased perhaps less than might have been expected to a level of 56% in 2020. By October 2021, 47% of patients had returned to a dental practice after the nationwide lockdown ease. However, half had not done so yet, meaning that they had not seen a dental professional at all for 18 months or more.

LaingBuisson predicts the market to continue an upward growth by an average of 2-3% in nominal terms in the next three years. This will mainly come from more spending on private dentistry, though much depends on the strength of the UK economy, and spending on NHS dentistry is expected to fall in real terms.

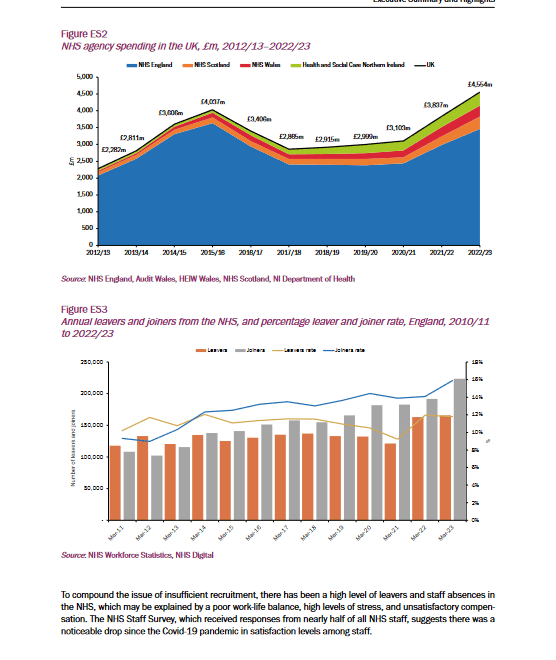

Challenges for the dentistry market are still focused on recruitment and retention. Providers continue to report challenges in the recruitment of dentists and dental care professionals. Some providers have reported labour shortages, resulting in the undershooting of NHS contracted activity, and an increased reliance on locum dentists. The shortage is affecting all roles, not just dentists. This comes at a time when a new NHS dentistry contract model, which aims to improve prevention and focus on patient outcomes, continues to be tested after many years of planning.

A positive outcome from the latest analysis showed that consolidation strengthened the market with several equity investments and transactions. This includes the recently announced merger of Portman Healthcare and Dentex.

“The structure of dentistry supply in the UK is a crucial determinant of demand behaviour. The majority of patients currently access dental services for NHS dentistry, and the minority access private dentistry as self-payers or through dental cover plans. Over time, shifts in dentistry supply has seen more dentists provide private dentistry, chiefly as more dentists have sought remuneration and working conditions of private dentistry over NHS dentistry.

“It is also the case that many more patients on the NHS are opting for private treatments as an upgrade to their NHS course of treatment. Going forward this shift to private dentistry supply is expected to continue as more dentists prefer working practices offered through private dentistry, and patients seek wider treatment options to suit their needs.”

Liz Heath and Keith Pollard

– Report authors

Published: 28 November 2022 (240pp)

£1,330.00 – £3,330.00

Related products

-

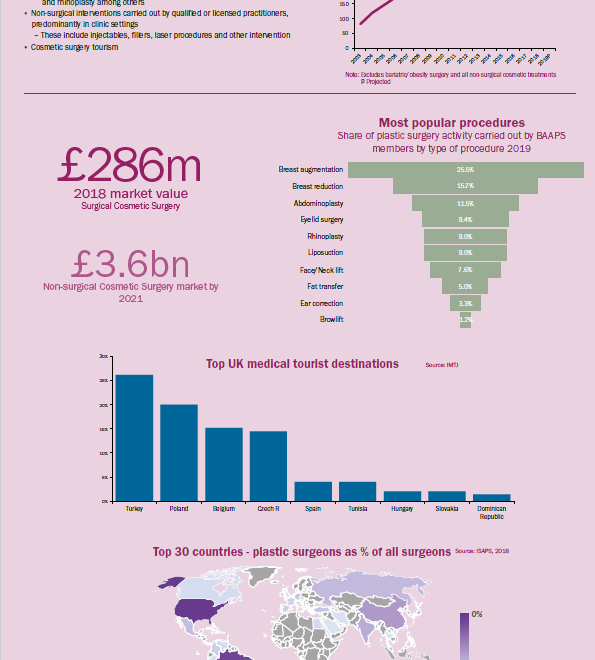

Cosmetic Surgery UK Market Report 2ed

£895.00 – £2,238.00 Select optionsWhat the report includes The impact of Covid-19…

-

Temporary Recruitment and Staffing: Healthcare 1ed

£995.00 Add to basketWhat the report covers Overall market value, and…

-

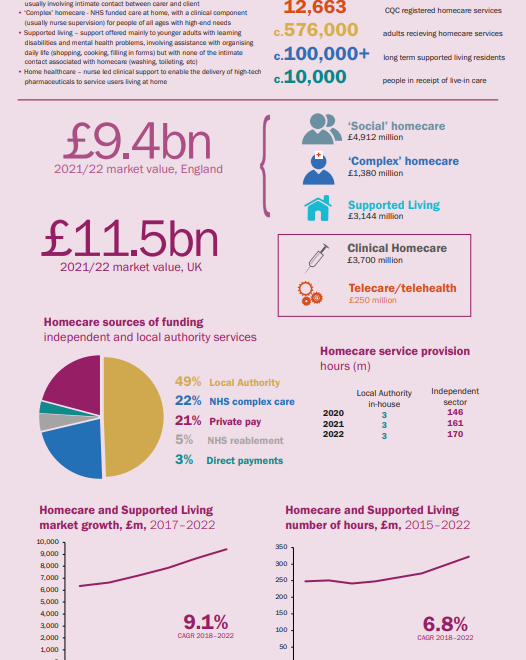

Homecare and Supported Living UK Market Report 5ed

£1,495.00 – £3,695.00 Select optionsWhat the report covers Market Politics and Regulation…