Adult Specialist Care UK Market Report 6ed

What the report includes

- Market

- Politics and Regulation

- Payors

- Major providers

- Investors

- Staffing

- Market Potential

- Appendices

Glossary

Regulators

Trade bodies and associations

Major provider profiles

Historical context

Financial appendix

Who is the report for

- Operators of residential care and nursing homes

- Homecare agencies and providers

- Nursing agency operators

- Local authority commissioners

- CCG commissioners

- Directors of adult social services

- Care advisors

- Banks and investors

- Management consultants

- Business advisors

- Long-term care insurance providers

- Central government

- Think tanks

- Policy writers

What You Get

- Print package – Single-user Printed Book

- Digital package – Multi-user Digital PDF and Data in Excel + Printed Book

Want to know more? Our sales team can help.

Call: 020 7841 0045

Email: [email protected]

Supported living has emerged as the primary choice for adult specialist care services

The sixth edition of LaingBuisson’s Adult Specialist Care UK Market Report is vital reading for anyone involved in social care for adults under 65, be they a provider, a commissioner, an investor, an advisor or a policy maker. Written and researched by leading market commentator, William Laing, this industry standard report provides unique insight into all areas of the market, including funding, operating models, future prospects and supply and demand.

The report covers all aspects of social care for younger adults and LaingBuisson estimates the UK market to be worth £14.5 billion (2021/22), with the top four care groups contributing only 7.2% of the total revenue in this unconsolidated market. This includes services for people with learning difficulties, mental health issues, substance misuse problems and acquired brain injury, and comprises both residential and non-residential settings.

The report reveals a rising preference for supported living over care homes. Clients, families, and councils increasingly choose supported living over care homes due to its greater independence and personalised care. This has resulted in almost 95% of adult specialist care services being provided by independent sector organisations. These organisations operate in a competitive market funded primarily by local authority social service departments. Supported living meets the preferences of service users and their families while offering cost advantages to cash-strapped councils by shifting property costs to central government-funded Housing Benefit.

Workforce availability remains a significant challenge. Initially, the pandemic brought in temporary staff from other sectors, but as the economy reopened, this trend reversed. To fill the gaps, social care employers have turned to hiring overseas workers with the help of relaxed immigration controls. However, the persistent workforce shortage remains a major obstacle in meeting the rising demand for care.

As anticipated, the health and social care sector has undergone extensive digitalisation due to the pandemic. This shift is expected to improve the efficiency of commissioning and provision of social care while enhancing safety and quality of care.

Report author, William Laing said:

“Against the background of a modest real terms expansion of the funding envelope for adult specialist care. Overall, spending on supported living is expected to continue growing its share, as registered residential care services for less highly dependent service users continue their slow migration to supported living settings. Most service users and their families prefer supported living to residential care, and this is reinforced by the financial advantage to local authorities of shifting property costs onto central government funded Housing Benefit.

“Over recent years, public policy has consistently supported the change in the balance of care. The government’s 2018 announcement that it will continue to fund supported accommodation rents through the welfare system (Housing Benefit) and will not subject rents to mainstream Local Housing Allowance (LHA) caps with discretionary top-ups, has effectively de-risked future rental streams, which long-term investors rely on to justify investment.”

Published: 7 July, 2023 (511pp)

Sponsored by

![]()

£1,495.00 – £3,695.00

Related products

-

Temporary Recruitment and Staffing: Healthcare 1ed

£995.00 Add to basketWhat the report covers Overall market value, and…

-

Childcare UK Market Report 16ed (with Covid-19 updates)

£895.00 – £2,995.00 Select optionsWhat the report includes * NEW * Coronavirus…

-

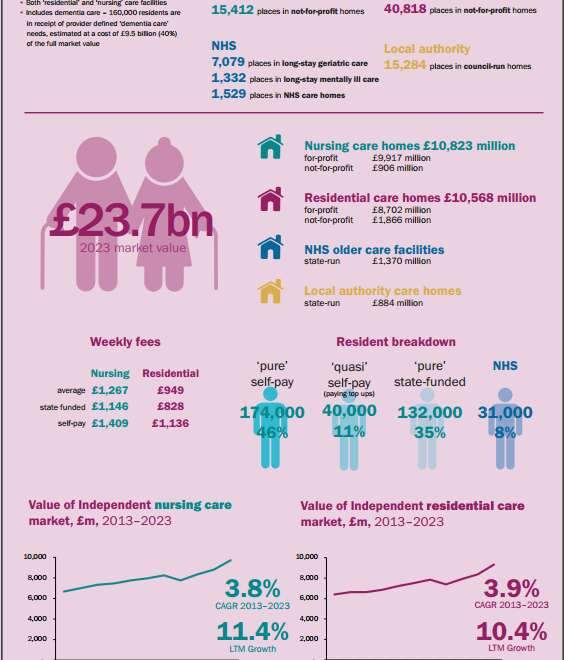

Care Homes For Older People UK Market Report 34ed

£1,295.00 – £3,950.00 Select optionsWhat the report covers Overall market value, and…